- Alekhlas Company for Trade and Export

- 00201558788096

- 00201205396886

- info@alekhlas-company.com

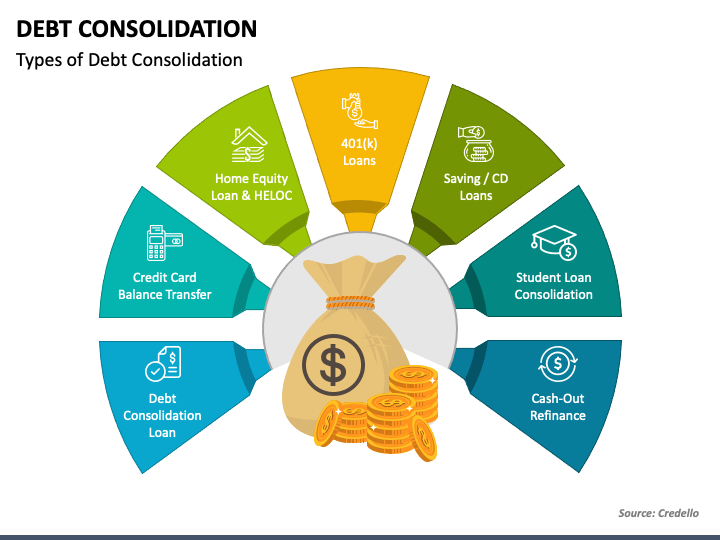

When the weight of multiple credit‑card balances feels heavier than a backpack, many borrowers reach for debt consolidation as a lifeline. Yet, not all consolidations are created equal—APR differences can mean the difference between sinking and staying afloat.

A low Annual Percentage Rate (APR) is the heart of any successful consolidation strategy. Think of it like a boat’s engine: the more efficient it is, the faster you reach your destination with less fuel burned. In financial terms, a lower APR reduces monthly interest charges and shortens repayment timelines.

To illustrate, the BankRate guide shows how a personal loan with a 6% APR can outperform multiple credit cards averaging 18% APR.

Traditional consolidation methods—visiting banks, calling lenders, and juggling paperwork—have long been laborious. Enter online marketplaces that streamline the process into a single application, matching borrowers with competitive offers from dozens of lenders.

For instance, Lending Match launched a platform that allows consumers to submit one loan application and receive real‑time offers from up to 35 lenders without hard credit inquiries. The result? Transparency, speed, and often lower APRs.

Not every loan or credit product fits every borrower’s needs. Consider these key factors before signing on:

| Feature | Why It Matters |

|---|---|

| APR | Lower rates reduce long‑term costs. |

| Term Length | Shorter terms mean higher payments but less interest. |

| Fees | Origination or prepayment penalties can erode savings. |

| Lender Reputation | A trustworthy lender ensures smooth service and fair terms. |

Financial experts recommend comparing at least three different offers. Tools like Money.com’s comparison charts provide a side‑by‑side view of rates, terms, and lender ratings.

Unsecured personal loans are popular because they don’t require collateral. If you have good credit (typically 700+), you may qualify for APRs in the low‑single digits—a sweet spot for debt consolidation.

However, borrowers with less-than-perfect credit might find secured options, such as a home equity loan or line of credit, more accessible. These products often come with lower rates but tie your borrowing power to the value of your property.

A recent case study from BankRate followed a borrower named Maya. She consolidated $12,000 of credit‑card debt into a personal loan at 7% APR over three years.

Maya’s story underscores how strategic consolidation can ripple into broader financial health.

Beyond the mechanics of loans, understanding budgeting principles is crucial. Resources like BankRate’s home‑equity guide offer insights into leveraging assets responsibly.

Workshops, webinars, and local credit counseling agencies can further empower borrowers to manage debt proactively. The U.S. Treasury’s consumer debt FAQ remains a reliable starting point for policy updates and best practices.

While many lenders provide legitimate, low‑APR options, some schemes can be predatory. Watch out for:

Always read the fine print and verify lender credentials through state licensing boards or the Consumer Financial Protection Bureau (CFPB).

Digital tools can simplify comparison shopping. Platforms that aggregate loan offers—like the one launched by Lending Match—allow you to filter by APR, term, and lender rating in real time.

Moreover, budgeting apps that sync with bank accounts can track repayment progress, ensuring you stay on course without manual spreadsheets.

If you’re ready to explore low‑APR consolidation options, Jetzloan offers a streamlined application process that connects borrowers with competitive lenders across the country. By leveraging Jetzloan’s marketplace, you can compare multiple loan offers in seconds and select the one that best fits your financial profile.

With transparent terms and a focus on borrower education, Jetzloan helps you make an informed decision—whether you’re aiming to pay off credit‑card debt, refinance a student loan, or consolidate various obligations into a single manageable payment.

The process typically takes less than 15 minutes, freeing you to focus on budgeting and financial planning.

The debt‑consolidation landscape is evolving rapidly. Key trends include:

Staying informed about these developments can help borrowers navigate offers more effectively and avoid pitfalls that arise from rapid market changes.

Debt consolidation is often the first step toward financial stability. The next phase involves disciplined budgeting, emergency savings, and continuous credit monitoring.

By maintaining a clear view of your obligations and actively managing them through tools like Jetzloan and reputable budgeting apps, you set the stage for lasting fiscal health—transforming debt from a looming storm into a manageable breeze.